<>

When starting as a freelancer, one of the issues that must be specified will be the correct preparation of an invoice with a autonomous invoice model. It is an essential document where the information necessary to execute a transaction, or make the purchase of goods or services will be reflected.

The delivery of invoices to clients will also allow the opportunity to develop the corresponding annotations in the sales and results books, which will be the accounting basis for calculating the taxes to be paid.

The non-issuance of this type of document in the appropriate cases will cause the self-employed to incur an underground economy, and may face a tax penalty for said fact.

Invoices must be consecutively numbered and kept as a copy of the issues made. The VAT and personal income tax percentages corresponding to the activity carried out must be included in their calculations.

On repeated occasions, the self-employed have doubts about the concepts to be handled, as well as about the data and requirements that must be met in order for a document of this type to be prepared in accordance with current regulations.

If this subject is not understood and mastered well, it is almost certain that the self-employed will end up having problems with the Treasury.

Let's go over some essentials to consider.

Invoice for freelancers: Data to include

Para que una factura be válida, deberá incluir datos mínimos indispensables.

In the case of not reflecting decisive information, or if any of the exposed data has errors, it will be necessary to issue a corrective invoice.

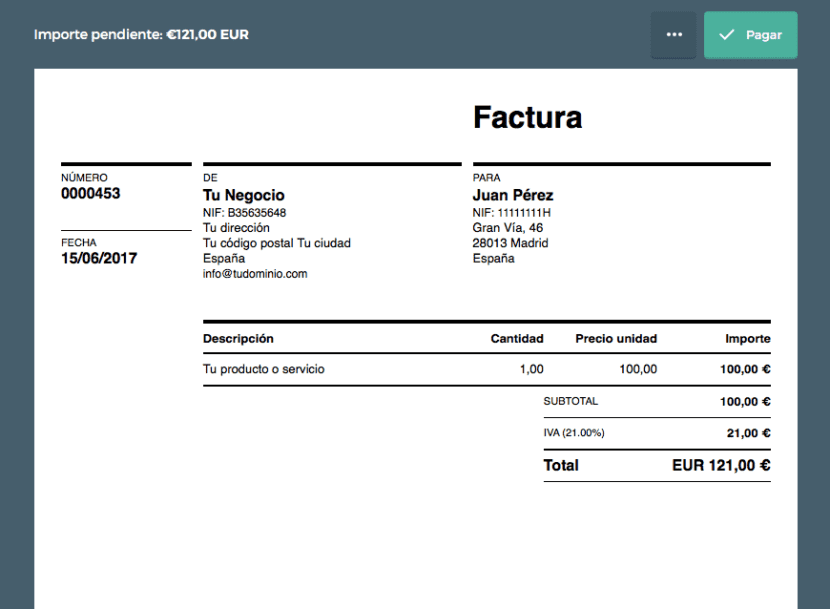

The main sections that the document will have will be the following:

- Details of who issues the invoice

- Details of who receives the invoice

- VAT rate (if applicable)

- Total amount to pay

- Porcentaje de retención en el impuesto sobre la renta de las persons físicas (si corresponde)

- Date of execution of operations

- Invoice issue date

- Data related to the operation in question

- Invoice number

- Tax rate (if applicable).

At data of who issues the invoiceInformation such as the name and surname of the person, their full business name, the NIF plus their address (NIF) will be included. In the information of who receives the invoiceIf the recipient of the same is a natural person, their name and surnames, business name if it were a company, address and NIF will be included.

Referring to the operation in question and its description, it is necessary to detail complete information in order to establish the taxable base of the tax.

The totalized amount of the consideration will be included including the unit price without taxes of each operation, in addition, discounts or rebates must be included, "if applicable", which are not included in the unit price.

In that invoice numberIn the same way as in the series, the numbering must be successive and continue in the respective order with the date of issue indicated. The invoices that are issued must be numbered in consecutive order; even though a new series usually begins each year. Invoices should not be numbered monthly by series.

Different series could be created in the event that there are several establishments, operations of a different nature are carried out or in cases of rectification of invoices.

East type of rectifying invoices They should not be issued with the same number and series as the original invoice. Both types are different bills and should not be mixed.

Invoice templates

There are different types of invoice model for freelancers.

- Invoice model without VAT for freelancers and SMEs

- VAT invoice template for the self-employed and SMEs

- Invoice model with VAT and personal income tax for the self-employed and SMEs

- Simplified invoice model for freelancers and SMEs

- Intra-community billing model for the self-employed and SMEs

- Invoice template for dependent self-employed

Let's specify some important information for some of these models.

Invoice model without VAT for freelancers and SMEs

As to invoice model without VAT for freelancers and SMEs, It must be recognized that there will be types of professional activities and products exempt from applying VAT.

It is essential to understand that making an invoice without VAT will not be the same as not making an invoice. Although the activity is exempt from VAT, it must be prepared and declared personal income tax.

Some of the products and activities that are exempt from VAT are the following.

Medical or sanitary operations will be included, in this circumstance veterinary and dental services for aesthetic purposes. Educational services; Financial and insurance operations; Non-profit sports, social and cultural services. Real estate products; Second-hand purchases and rentals; Postal services; Lotteries and bets.

Simplified invoice model for freelancers and SMEs

Regarding the simplified invoice model for the self-employed and SMEs, in 2013 this invoice was introduced. It replaced the ticket that was issued in all operations up to € 3,000 (VAT included).

From that moment the ticket is not accepted as an accounting document justifying an expense and the simplified invoice may be issued by freelancers in small operations that do not exceed € 400 (VAT included), if a corrective invoice or for activities in which it was frequent to issue a ticket, if the amount does not exceed € 3,000 (VAT included).

The activities that allow issuing a simplified invoice will be:

- Transport of people and their luggage

- Use of toll roads

- Retail sales

- Hairdressing services - beauty salons

- Dry cleaning and laundry services

- Hotel and restaurant services

- Ambulance services

- Service and use of sports facilities

- Sales or home-based services of the consumer.

- Services provided by discos and dance halls

- Parking and parking of vehicles

Sobre los datos y contents que debe tener este tipo de factura simplificada, podemos resumir It must be explicit regarding the sender, his name and surname, business name and NIF. The tax rate and, optionally, the expression "VAT included"; Date of the operation, if different from the date of issue. If the invoice is rectifying, include the reference of the rectified invoice. Identification of the goods that are delivered or the services provided; Total consideration; Number and series; Expedition date.

In the following circumstances: mention of «Special regime for used goods«; in exempt operations, reference to regulations; to mention "billing by recipient«; to mention "Special regime for travel agencies”.

Intra-community billing model for the self-employed and SMEs

En el modelo de factura intracomunitaria para autónomos y pymes, si se emite una factura para un client en un país de la Unión Europea, el IVA que se aplicará dependerá de si se trata de un bien o servicio.

If a good is invoiced to a company or autonomous, the invoice is made without VAT if the client is registered in the «Registro de Operadores Intracomunitarios» – ROI. If a good is invoiced but it is to a final consumer, the VAT of the country applied to that good will be applied. It will involve registration in the country, with the exception of not exceeding the sales tax limit established by the tax authorities of the client's country.

In the case of billing a service, either to a company or a self-employed person, an invoice is made without VAT, deductible VAT for the goods and services used to carry it out.

If an end consumer is being invoiced, the applicable Spanish VAT is applicable, except for television and electronic services, telecommunications and radio broadcasting, in which the applicable VAT is that of the client's country.

Invoice template for dependent self-employed

There he is dependent self-employed (economically dependent self-employed) - COMMERCE. It is a self-employed person who will invoice at least 75% of the income received by the same client.

For this reason, Social Security grants them a type of protection to avoid abuse. They must invoice following the specific regulatory norms and since they are invoicing as self-employed, they will be subject to the same tax obligations as any other self-employed person: in other words, quarterly VAT self-assessment on invoices, quarterly payments on personal income tax, etc.

In order to bill, this type of self-employed person must pay attention to two fundamental aspects.

The first will be the VAT rate that you will apply to your client. This can be 21%, 10% or 4%, and will depend on the service or product in question that is billed. The second will be the withholding of income tax that you will be applying to your client for being a company or professional. The retention will be 15%, but new freelancers will be able to apply for 7% during the first two years.

For the rest, you must pay attention to the different mandatory contents of an invoice sheet.. We talk about specific customer data, name, business name, NIF or CIF, address. Develop the description of the service or product being offered. The price of services and products. VAT rate to apply. Tax quota, which will be the part of the amount that will correspond to VAT. Total amount, IRPF Withholding, which is subtracted from the tax base.

To understand what conditions a dependent self-employed must meet, and before entering into any contract, we suggest reading Section III of the Employees Statute, dedicated exclusively to dependent self-employed persons.