<>

Elegir entre una hipoteca fija o variable puede ser complicado si no estamos seguros de dónde estamos. Es el problema de muchas persons al momento de firmar una hipoteca, decidiendo entre una y otra. En realidad, Both options have their good and bad quirks., but everything will depend on the context in which the person is. The context that can end up influencing this decision the most may be monetary policy, available capital and an emotional predisposition to risk or not.

Existen muchas webs que hablan de las ventajas y desventajas de obtener una hipoteca fija o variable. Puede ser un poco confuso para las personas a las que les gustan más las letras o las imágenes y no tanto los números. Es por ello que el reclamo de este post es que, sin descuidar lo que es lo más rentable o exitoso, acercarlo un poco más al público en general y hacer que se entienda bien qué esconden esos intereses mediante gráficos y ejemplos. De esta dinámica, ayude a establecer según su perfil qué hipoteca prefiere.

Main differences between fixed or variable mortgage

Assuming that we all know what a mortgage is, we are going to see the main differences between one mortgage and another.

- Fixed mortgage: Its main advantage is that we will know what quota is going to reach us each month until maturity. A fixed mortgage maintains a fixed interest rate for the years it will be in effect. So, if you are at 3% (as an example), we know that each year we are going to pay 3% of the outstanding face value (“what remains to be paid”). In other words, if at 4 years we have 90,000 euros outstanding, that fifth year we would pay 2,700 euros of interest (the 3% of the 90,000 euros that are pending). As it is a fixed rate mortgage, the bank will generally apply a higher interest than a variable rate mortgage.

- Variable mortgage: Its main advantage is that at the time of signing it, the interest that will be charged on the mortgage will be less than that of a fixed mortgage. However, a variable mortgage as the name suggests does not maintain a fixed interestInstead, it is related to a benchmark index, in the case of Spain the Euribor. That means that if the Euribor does not move, or goes down, our mortgage will stay or go down. If, on the other hand, it rises, the % of interest that will be applied to us will increase when the interest on the mortgage loan is renewed. As an example, we have spent the last year paying 0'80% of interest on our loan and we have 90,000 euros left. If it is maintained, next year we will pay 720 euros (0.8% on the 90,000 euros). If a 0.20% falls, we would stay with 0.6% (0'80-0'20 = 0'60) and we would pay 540 euros of interest next year (0.6% on the 90,000 euros). But, and this is what discourages people, if an 1% suddenly went up, next year we would pay 1,620 euros (and it could continue to go up year after year).

A fixed or variable mortgage depending on the moment

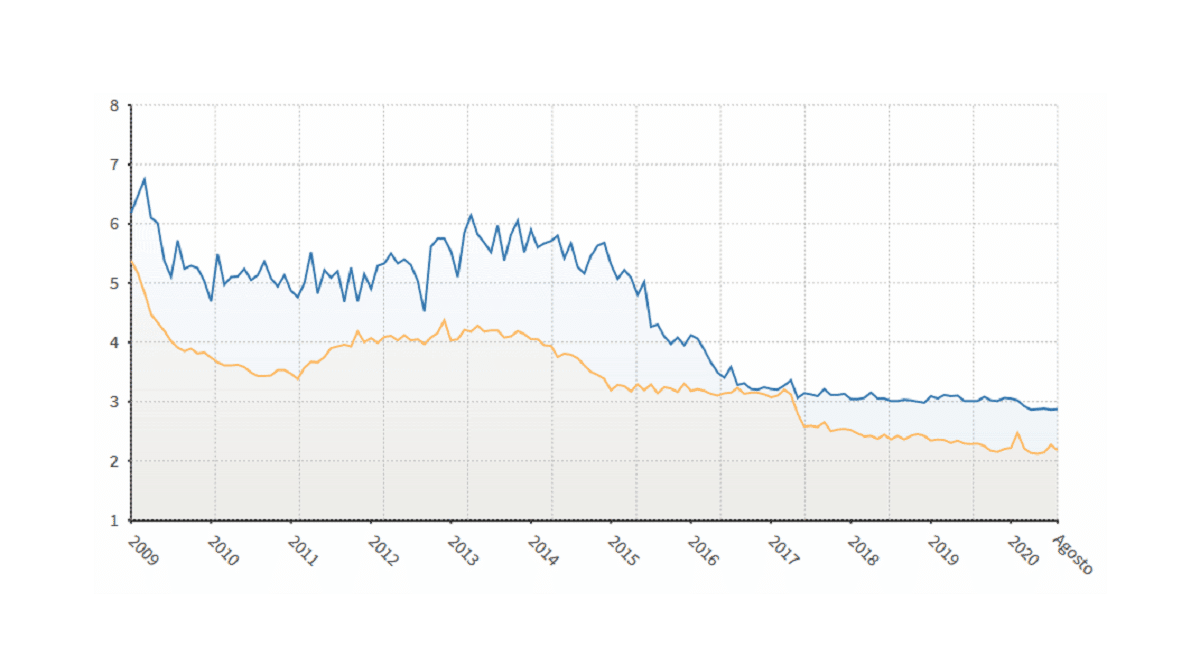

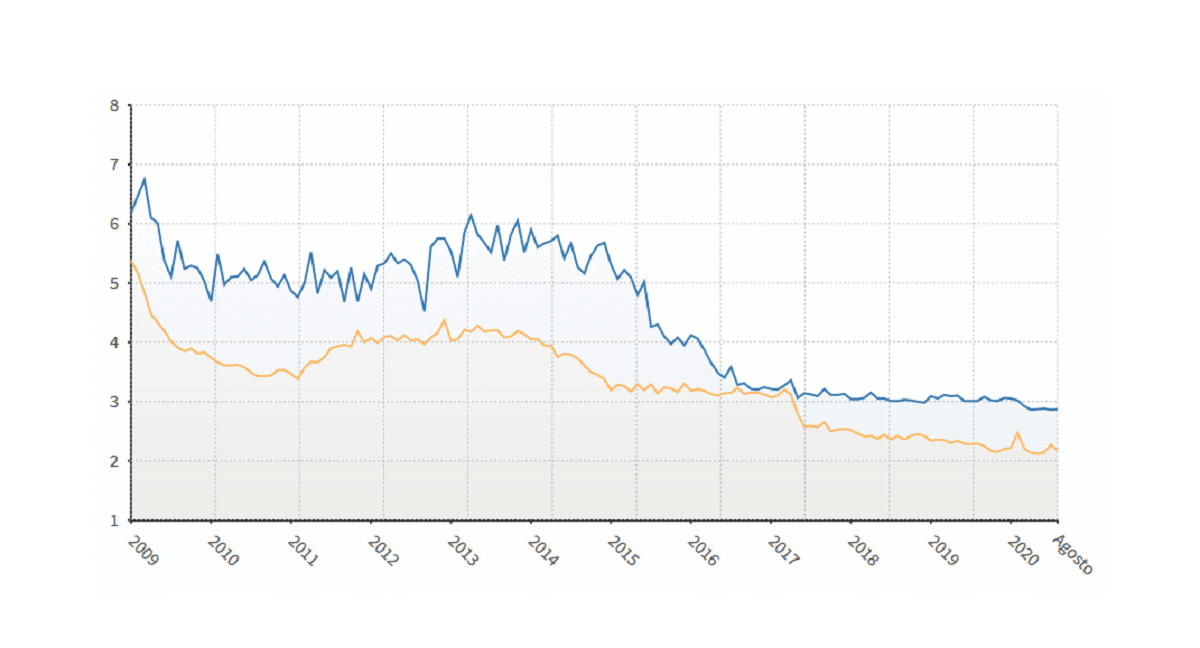

Este gráfico corresponde al tipo de interés medio al que se han suscrito las hipotecas en los últimos años. Hipotecas fijas en azul e hipotecas variables en amarillo. Los datos los proporciona el INE, y una muy buena Web de la que extraer estos datos de un plumazo gracias a sus gráficos es epdata.es which I recommend for the large amount of information it provides.

The fall in the Euribor has accompanied the fall in interest on mortgages, as we can see in the graph. The fact that interest rates reached levels below the 0%, has pushed many people to prioritize the security of the fixed mortgage over the variable one. In fact, In 2020, more mortgages were signed at a fixed rate than at a variable rate. It even made it easier for many people to change their mortgage from variable to fixed. The main reason, to protect yourself from possible interest rate hikes. Increases that have not arrived either, as a mechanism to improve consumption and make credit flow is to keep rates low.

Related post:

Why is the Euribor negative?

According to monetary policies on interest rates

Es cierto que la pandemia ha puesto patas arriba muchas previsiones económicas, pero si nos centramos en el pasado y los principales mecanismos para mejorar la economía a través del BCE, los tipos de interés no deberían tener subidas fuertes, al menos a corto y medio plazo. Esto quiere decir que sería más interesante pagar una hipoteca con interés variable, especialmente si es por unos años. No obstante, cuanto más largo be, más justificado sería adoptar una tasa fija para protegerse contra posibles aumentos de las tasas de interés.

Something that we must establish is our position and the risk that we can take (financially and emotionally), since a variation of the 1% carries hundreds of euros in all the years of a mortgage. At the same time, it should be remembered that at the beginning is when most of the principal is paid. As the years go by and it is amortized, that interest decreases in proportion to the capital contributed in each letter.

According to the capital available to the buyer

We imagine that we have a buyer who has more capital than he contributes. In the event of further increases, the capital could always take a step forward. Meanwhile, and in the event that interest continues to fall, or increase, but only slightly, you could choose not to use that capital. Your preferences could even be investment preferences, which would be more interesting as long as it provided you with a higher return on invested capital than the interest you pay on your mortgage.

The provision of liquidity can provide insurance against rises at the same time. If you have money that is not used and the interest rate of a variable mortgage goes up a lot, it would not be a bad idea to amortize part of the principal.

Another scenario would be that of a person who wants to be in control of their expenses, and that is less than the security of knowing in advance what they are going to pay. In this dynamic, a fixed mortgage would be the ideal option.

Emotional predisposition to risk

If we are people risk aversion, a fixed rate mortgage would be the best option. Fundamentally if we see news on television that interest rates are going to rise, and they are going to affect mortgages referenced to the Euribor. On the other hand, if such news does not make us nervous, and we consider that future cuts in the Euribor may take place and thus benefit us in our mortgages, the variable would be a better option. At the same time of being a percentage lower than the average at the time of signing.