<>

This tax in Spain constitutes the basis of the Spanish indirect tax system, VAT means Impuesto sobre el value added. Vamos a aclarar los tipos de IVA que se cobran en España.

Creada en 1986, esta a petición de la Comunidad Económica Europea, sustituyó a la Tasa de Traffic Empresarial y fue reformada a nivel comunitario en 1992 con la finalidad de adecuarla al conocido mercado interior dentro de la Unión Europea que provocó la supresión de la controles fronterizos.

Law 37/1992 is the fundamental legislation that regulates the tax.

The tax over the value addedUnlike what happens with other indirect taxation systems, it is neutral towards companies, since it does not entail expenses or income for them, insofar as the goods acquired in production or distribution are always used in their procedure. of production or commercialization.

This neutrality is removed the moment the final consumption of the goods.

The responsibility for the correct application of the VAT tax mechanics rests with the employer or professional, who becomes a collector for the State of the part of the tax that corresponds to the value caused or added in its production stage.

Consequently and therefore, it is he who is obliged to self-assess said tax through the presentation of the corresponding quarterly or monthly returns.

VAT is the main indirect tax in Spain and almost all over the world.

Three types of VAT coexist in our country

- general

- Reduced

- Super reduced

The function of VAT is to tax the consumption of all citizens.

It is a common tax for everyone and does not depend on your income, your job or your work / personal situation.

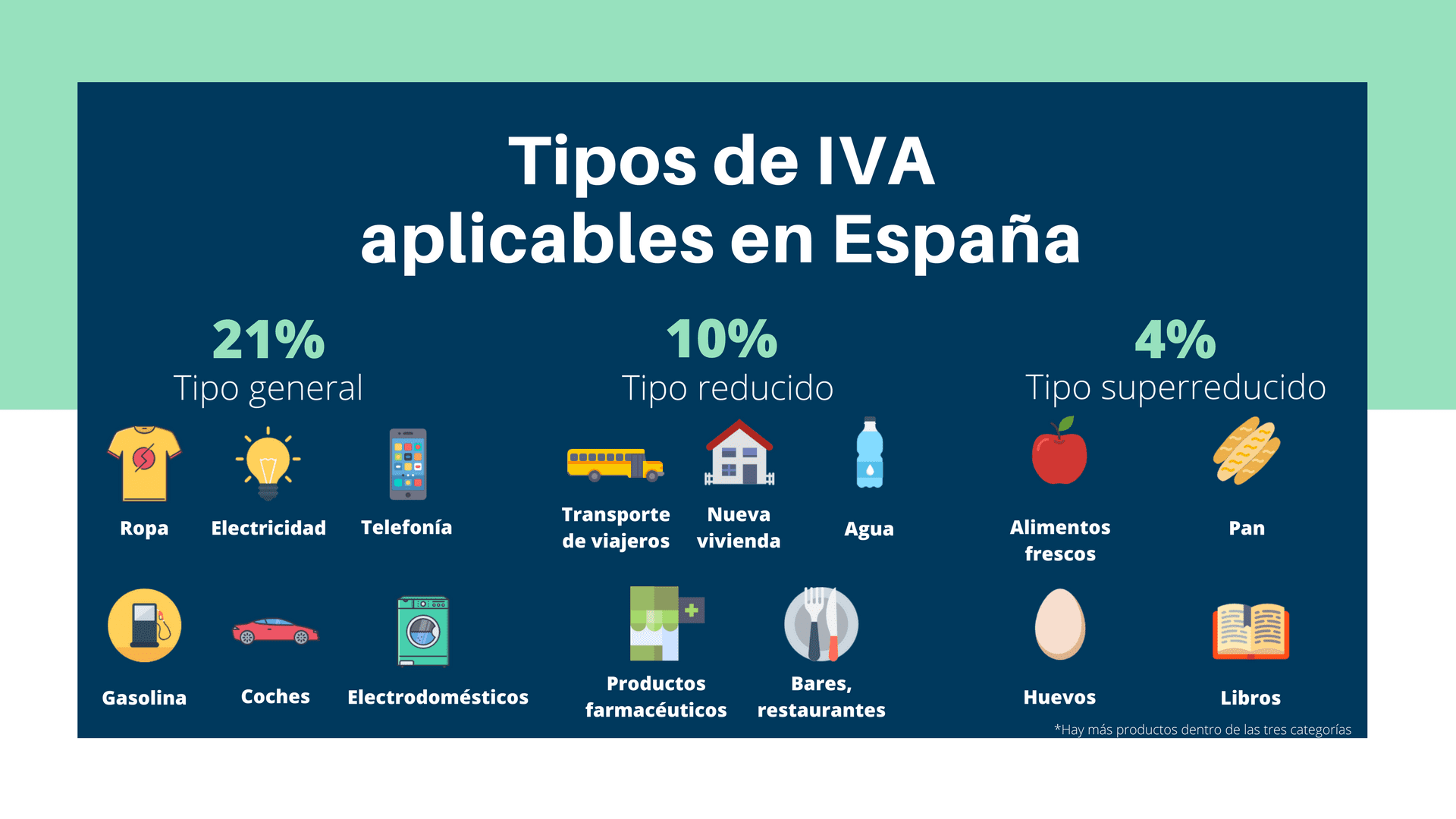

After the reform of the VAT legislation (Value Added Tax) has been carried out through the approval of the ley of the general state budgets for the year 2010, on July 31 of last year and after the last increase in VAT rates in Spain, the tax remains with this percentage:

- General type: twenty one%

- Reduced rate: 10%

- Super reduced type: 4%

This tax is applied to tax all goods and services that citizens consume.

The VAT tax differs from personal income tax in that it is not applied directly on the taxpayer's income, but on any consumer good through its manufacturing and distribution phases and, therefore, rewill ultimately affect the price paid by the consumer.

Parts of VAT

It is feasible to divide this tax into three parts:

- Tax base: This base is constituted by the total amount of the consideration of the operations subject to the tax.

- Tax rate: Refers to the percentage applicable to each consideration subject to tax, with which the amount of the same can be established.

- VAT rate: This is the result of applying the tax rate added to the tax base.

How is the final VAT amount obtained?

The VAT is an indirect tax, which means that as a product or service goes through different parts of its manufacture or distribution, the amount will be added.

The consumer is responsible for paying this tax in full at the time of purchase.

As a general rule, the most basic and necessary products have the lowest VAT and the products that are not essential are those that are taxed with a higher percentage.

The percentage of this tax depends directly on the type of product or service.

Just to recap what has already been mentioned so far in the previous paragraphs:

- VAT is added throughout the entire production chain: From this dynamic, every company that intervenes in the procedure includes the VAT percentage corresponding to its services. But, who in conclusion pays the VAT is the one who consumes or contracts the product or service.

- Companies act as tax collectors: Every three months they must pay the Treasury the difference between the VAT they bear and the one they charge. To put it in more understandable words:

Every company and professional charges VAT on their invoices and enters that VAT added to the cost of their product and at the same time has to pay VAT for the services they hire.

- The VAT you enter is not yours, but the Tax Agency: This requires companies to return it quarterly.

This requirement is known as VAT returns and the Treasury forces you to return the difference between the VAT that you have entered and the VAT that you have paid, also known as deductible VAT and which must always be related to your economic activity.

General VAT

The general VAT in Spain is 21% even when before it was 18%.

As its name suggests, it is the general tax that applies to most goods and services that consumers buy:

- Jewelry

- Home appliances

- Books

- Clothing

- Toys

Tras la reforma fiscal, se han agregado a este grupo algunos servicios que antes tenían un IVA más bajo, como a modo de ejemplo peluquerías, servicios funerarios, asistencia sanitaria o servicios prestados a persons físicas que practican deporte.

It is also necessary to point out the increase from 8% to 21% of the entries to

- Theaters

- Cinemas

- Shows

- Concerts

- Zoos

- Commercial premises and buildings destined for demolition

- Entrance to discos and nightclubs.

Reduced VAT

The reduced VAT is 10%, even though before the tax reform it was 8%.

This VAT rate applies to all food usually, so the list is quite extensive. It should be noted that some foods have a super-reduced type. The reduced VAT includes all food for human and animal consumption.

The main exclusion is tobacco., whose VAT is 21% as well as the alcoholic drinks, which were previously in this section.

also I know include the goods for

- Agricultural or forestry activities

- Water

- Medicines for animal use

- Eyeglasses

- Contact lenses

- Medical devices

- Transportation of passengers and luggage

- Hostelry

- Food services to eat on the spot

- Public street cleaning services

- Entrance to libraries

- Galleries

- Museums

Super reduced VAT

In Spain there is a VAT rate, the super-reduced VAT, which is only 4%.

This type of VAT is intended for basic products:

- Bread

- Dairy products

- Flour

- Eggs

- Fruit

- Vegetables

- Vegetables

- Legumes and cereals

- Books

- Newspapers

- Journals

- Medicines for human use

- Vehicles for people with reduced mobility

- Prosthetics and daily assistive devices with disabilities

- Officially protected housing

- Leases or telecare services.

VAT worldwide

VAT is the most widespread tax along with personal income tax. and the Corporation Tax.

Other fees and taxes such as the IBI or the Registration Tax are not so universal.

Each country adapts the VAT to its own reality, which translates into an amalgam of different percentages and even different types of VAT.

Even within the European Union itself there are different types of VAT and regions to which exceptions apply, such as in Canary Islands, where the IGIC or General Indirect Tax of the Canary Islands governs.

Here is a table to compare for each country.

| Country | General type | Reduced / super reduced rate |

| Germany | 19% | 7% |

| Austria | twenty% | 10% (12% parking) |

| Belgium | twenty one% | 6% (12% parking) |

| Bulgaria | twenty% | N / A |

| Cyprus | 19% | 5% |

| Croatia | 25% | 10% / 5% |

| Denmark | 25% | N / A |

| Slovakia | twenty% | 10% |

| Slovenia | 22% | 9,5% |

| Spain | twenty one% | 10% / 4% |

| Estonia | twenty% | 9% |

| Finland | 24% | 14% or 10% |

| France | twenty% | 10% or 5.5% / 2.1% |

| Greece | 2. 3% | 13% / 6,5% |

| Hungary | 27% | 18% or 5% |

| Ireland | 2. 3% | 13.5% or 9.0% or 4.8% or 0% / 0% |

| Italy | 22% | 10% / 4% |

| Latvia | twenty one% | 12% or 0% |

| Lithuania | twenty one% | 9% or 0.5% |

| Luxembourg | fifteen% | 6% / 3% (12% parking) |

| malt | 18% | 5% |

| Netherlands | twenty one% | 6% |

| Poland | 2. 3% | 8% / 5% |

| Portugal | 2. 3% | 13% or 6% |

| United Kingdom | twenty% | 5% or 0% |

| Czech Republic | twenty% | 14% |

| Romania | 24% | 9% |

| Sweden | 25% | 12% or 6% |

Zones without VAT or with limited VAT

| Country | Territory |

| Germany | Helgoland Island and Büsigen Territory |

| Spain | Ceuta and Melilla and the Canary Islands |

| France | Guadeloupe, Guyana, Martinique and Reunion |

| Italy | Livingo, Campione d'Italia and the Italian waters of Lake Lugano |

| Greece | Mount Athos |

| Austria | Jungholz and Mittelberg |

| Denmark | Territory of Greenland and Territory of the Faroe Islands |

| Finland | Aland Island |

| United Kingdom | Islas del Channel y Gibraltar |

VAT applied by the most important countries

| Country | General type | Reduced rate |

| Argentina | twenty one% | 10% |

| Andorra | 4,5% | 1% |

| Australia | 10% | 0% |

| Brazil | 12% | + 25% + 7% + 5% |

| Canada | 5% | 4,5% |

| porcelain | 17% | 6% or 3% |

| India | 12,5% | 4% or 1% |

| Japan | 5% | N / A |

| Mexico | 16% | 16% or 0% |

| Norway | 25% | 14% or 8% |

| Russia | 18% | 10% or 0% |

| Servia | 19% | 8% or 0% |

| Swiss | 8% | 3.8% or 2.5% |

| Turkey | 18% | 8% or 1% |

| Ukraine | twenty% | 0% |